#05: Veeva | $VEEV

Pharma's software monopoly, de-rated on the wrong read of AI

Veeva Systems

US: NYSE

Industry: Life sciences software

Market cap: $28,000 MM

Near-monopoly in its core categories (~80% in CRM)

System of record for pharma R&D: trials, regulatory, quality, safety

Outlines

AI makes drug discovery faster, but biology and regulators remain slow

More candidates mean more trials, filings, quality work and safety cases

Veeva is the default software layer for that regulated workload

Falcon could turn Veeva from workflow software into labor automation

High-quality founder-led business de-rated on seat-pricing fears

What people still miss about AI

I work at a quant firm, so let me start with the change I’m actually living through. It’s where this whole thesis starts.

Most people experience AI as something that answers. It explains, summarizes, drafts, and helps with almost anything you throw at it. A smaller group has already clocked the next step: it writes code. And once a machine can write code, it can build almost anything. Now put that ability inside a loop — let the model set itself a goal, write code to test an idea, read what comes back, and try again with a better guess — and it stops being something that merely responds and starts being something that probes. The step almost nobody is pricing in is the one after that: AI is starting to do research itself. It is learning to look for answers nobody has yet, instead of just repeating what we already know.

Research is a loop. You read, connect a few ideas, form a hypothesis, test it, look at what comes back, and go again with a slightly better guess. It is not a flash of genius. It is a grind of iteration. And the cost of one turn of that grind has collapsed. When something gets that much cheaper, you don’t do the same amount of it for less money. You do far more of it.

The point isn’t that the machine’s ideas are good. Most research ideas are bad, whether a human or a model produces them. The point is that generating, testing and discarding ideas has become cheap enough to do at scale, in a way no human team could match.

A good public example makes this concrete: DeepMind’s AlphaEvolve.1 It automates exactly the loop above: an LLM proposes candidate solutions, an automated evaluator scores them, the best ones survive and get mutated, and the cycle runs again. And it isn’t locked inside big tech: open-source versions like OpenEvolve already exist, so anyone can run the same loop.

What it produced is the part an investor should sit up for. Take matrix multiplication, a basic operation computers run billions of times a day. The best-known method for one version of it had stood unbeaten since 1969 — more than fifty years — and AlphaEvolve found a faster one.

“In 20% of cases, AlphaEvolve improved the previously best known solutions, making progress on the corresponding open problems.” — Google DeepMind2

This is not a chatbot being useful. This is research. We are looking at systems capable of generating entirely new knowledge and beating human specialists at their own game.

This paradigm shift applies directly to the biotech and pharma industries. As the cost of iterating through ideas collapses, the number of candidate molecules, assays and clinical protocols being generated and tested is going to explode.

The underlying raw capability keeps improving at an unbelievable pace. Anthropic, for instance, recently showed its Claude model reading NMR spectra (a standard way to identify a molecule’s structure) about as well as the specialized software chemists traditionally rely on.

The bottleneck just moves

Here’s the trap to avoid: assuming faster discovery means faster medicine. It doesn’t.

Drug development has always had two slow stages.

Discovery: finding a promising molecule.

Validation: proving in humans that it is safe and that it works, through years of clinical trials and regulatory review.

Both were bottlenecks.

AI attacks the discovery bottleneck. It does much less to the other one. A human trial takes as long as human biology takes; you can’t iterate your way out of a two-year safety readout, and a regulator isn’t going to approve a drug faster just because the candidate was found by a clever loop. So the bottleneck moves downstream. The slow, regulated, paperwork-heavy stage becomes the part that gates everything.

“Drug discovery is one thing. There is a lot of focus on that, and yes, that will get faster, but that is not the real bottleneck. The real bottleneck is the clinical trial, the experiment that is done in the human. We are always going to have to do those experiments in human, and human biology runs the same speed.” — Peter Gassner, founder & CEO. Q4 FY2026 earnings call, March 2026

This isn’t a futuristic bet. Discovery is already speeding up, and we have real cases to prove it. One AI-designed drug candidate recently reached the clinic in about 18 months instead of the usual four-plus years, and went on to pass its mid-stage trials. Others are clearing preclinical work in months rather than years.3

None of that proves an approvals boom. It proves something narrower and more investable: when discovery gets faster, more candidates pour into a funnel that was already slow, and each one drags the same evidence burden behind it.

More shots on goal do not mean more approvals on any predictable schedule. They mean more trials being run, more data to manage, more documents to assemble, more safety events to track, more correspondence with regulators, and ultimately more drugs to launch and sell. Most of that work is regulated, and it gets bigger precisely because the front end sped up.

AI makes discovery faster. The regulated work that follows doesn’t — it just piles higher.

I find this freeing as an investor, the same way the Weight Watchers thesis was. I do not need to know which molecule wins, which company reaches Phase 3 first, or which platform commercializes. I am not smart enough to call that. I only need to believe that the volume of this work goes up. And someone has to run it.

Veeva

That someone, for most of the industry, is Veeva.

Veeva started in 2007 with a single product: a CRM for pharma sales reps, built on top of Salesforce. But selling to reps was never the big prize. Over time, Veeva built its own cloud platform, Vault, and used it to push into a much larger and stickier market — the R&D side of drug development: running clinical trials, building regulatory submissions, managing quality, tracking drug safety.

That R&D business has already overtaken the original commercial one in revenue, and it’s still the faster-growing of the two.

My bet is that, over time, there may be a third leg that becomes even larger than both: agentic labor. Veeva selling the work itself, not just the software where the work happens. But more on that later.

Recently, Veeva began migrating its CRM clients off Salesforce and onto Vault, allowing the entire ecosystem to run on its own end-to-end stack. The transition has been slightly bumpy — a few clients used the migration to jump to Salesforce’s standalone product, fueling the bear case. I read it as short-term noise. Owning the full stack lets Veeva build AI natively into every workflow, worth far more over time than a couple of accounts it will likely win back anyway.

This deep integration makes Veeva incredibly difficult to replace. Switching costs in regulated software are brutal because the rules aren’t uniform: they differ by country, by agency, by therapeutic area, and the system has to encode all of it correctly. A mistake isn’t just a software bug; it’s a critical regulatory event. Veeva has spent fifteen years accumulating that knowledge, and it shows up in market share you almost never see in software — somewhere around 80% in its core CRM category, and the clear default in clinical. You do not rip out the system your trials and submissions live in, and certainly not mid-trial.

“We have 6 of the top 20 that have agreed to start all new trials on Veeva... this could be 3, 4, 5 years to get all the trials onto Veeva, but it’s happening.” — Peter Gassner

There’s a quieter tell of the moat that I like even more. Veeva is highly profitable and barely advertises: it spends far less on sales and marketing than other software companies and still compounds revenue in the high-teens to low-twenties year after year. A business that doesn’t have to buy its growth is one where the product and the lock-in do the selling.

Even without the AI angle, Veeva is the kind of business that almost never looks cheap: dominant niche, sticky, high margins, strong cash conversion and founder-led. The market has long known it, which is why Veeva almost always traded at a rich multiple. That’s exactly what makes today unusual — but price comes later.

Falcon: from seats to agentic labor

Now the objection everyone raises.

Veeva mostly charges per seat. If AI lets customers do the same work with fewer people logged in, the fear goes, a seat-based business shrinks as its customers get more efficient: AI becomes a headwind instead of a tailwind. It’s a real concern, and it’s a big part of why the stock has de-rated over the past several months.

There are two reasons I think the fear is overdone. The second is the actual thesis.

The first is mundane. A company that owns a critical workflow and creates real value almost always finds a way to charge for it; pricing follows value, with a lag. Veeva is already moving its AI features off pure seat pricing, and management has been explicit about how:

“You can imagine most likely that Falcon will be charged by the document... safety will be most likely charged by the case,” with Vault AI “usage-based on tokens.” — Peter Gassner, Q1 FY2027 earnings call, June 2026

The second reason is the part I’m genuinely excited about. Remember that growing pile of work. A surprising amount of it is the kind of task you’d assume software had automated years ago, which raises the obvious question: if it’s so routine, why are armies of people still doing it by hand?

Because it was never really routine.

Trial documents arrive as crooked scans and PDFs named differently by every site. Safety reports arrive as free text someone has to read and interpret. Regulatory questions come back in formats that do not fit neatly into a database. The work looks repetitive from far away, but up close it is messy, judgment-heavy and full of exceptions.

Ordinary software needs clean, structured inputs, so the messy front end stayed human. Reading the mess and applying a bit of judgment is exactly what modern AI can finally do, at least for a first pass, leaving the genuinely ambiguous cases to a person.

That is what Falcon is. Announced in May 2026, with early-adopter availability planned for late 2026, it is Veeva’s agentic platform for drug development, and its first agents go straight at this work: trial-master-file intake and quality control, drafting responses to health-authority queries, and safety case intake and triage.4

Veeva’s own case-intake demo is worth watching because it makes the whole idea concrete: one agent reads an incoming adverse-event report, pulls out the patient, drug and event and codes them; a second drafts the case narrative — the careful work a trained human used to do case by case.5

The reason this matters is that it points at a market Veeva doesn’t sell into today. Management is blunt about that:

“This is not a market we address today. We don’t play in that market today... [those agents] have to become users of our applications.” — Peter Gassner, Q1 FY2027 earnings call, June 2026

So the question stops being “how many seats” and becomes “how much work gets done.” If Falcon lands, Veeva starts charging for the work itself, not just the software around it — a slice of a labor budget, a far larger pool than it touches today. And if it doesn’t, the thesis still holds: the rising regulated workload carries Veeva as the system of record either way. Falcon is upside, not the reason to own the stock.

Veeva sells the software the work runs on. Falcon is the bet that it can sell the work itself.

When the founder is enough

Veeva is run by its founder, Peter Gassner, an engineer who built the platform and still runs it. I worry far less about an AI transition with someone who has spent his life building software and has real skin in the game than with a professional manager meeting agents for the first time in a McKinsey deck.

A small tell of how this company is run: Veeva raised about $7 million before going public, but only used about $3 million of that funding.

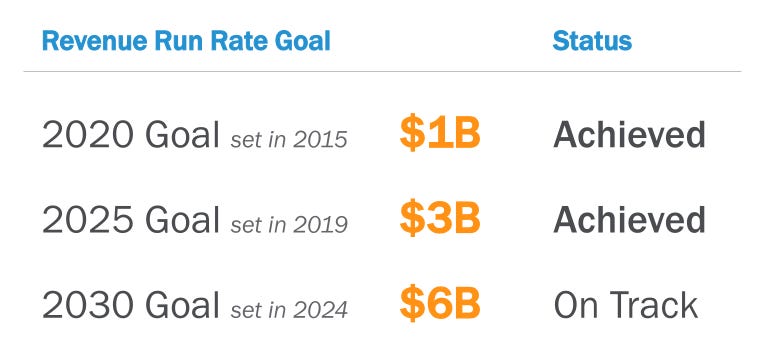

What I weigh most is his track record of saying what he’ll do and then doing it early. Gassner sets ambitious, multi-year targets, states them publicly, and beats them ahead of schedule — Veeva crossed its $3 billion run-rate goal early, and the next marker is $6 billion of revenue by 2030.

This is the same thing I admired in Ernie Garcia at Carvana: a founder who states an audacious long-term number and then quietly delivers against it. When you find management like that, you can lean on something more durable than any spreadsheet.

The price

I’ll keep this short, because the precise figure matters least. For most of its life, Veeva was expensive, and deservedly so. A business this dominant, sticky and cash-generative rarely trades cheap.

That’s what makes the current setup unusual. The stock has de-rated hard. On free cash flow — the right lens for an asset-light business that converts most of its profit to cash and sits on net cash rather than debt — Veeva trades at a fraction of its historical multiple, down from roughly 30x-40x toward the mid-teens.

The de-rate is the seat-and-AI fear, priced in. But if the thesis here is right, AI doesn’t shrink this business: it enlarges the regulated workload Veeva runs, and Falcon opens a market it doesn’t touch today.

The base case is simple. Veeva is doing about $3.2 billion of revenue run-rate today and management’s target is $6 billion in calendar 2030. At its 35%+ operating margin target, that implies about $2.1 billion of operating earnings power.

A 25x multiple on that is not demanding for a business with Veeva’s moat, margins and switching costs; it is still well below where the stock has traded for much of its life. That gets you to $52.5 billion. Against today’s roughly $28 billion market cap, that is already a very respectable outcome: close to a 2x over four and a half years, or a high-teens annualized return.

The balance sheet makes the setup better. Veeva has more than $7 billion of net cash and has authorized $2 billion of buybacks, so management has real room to retire shares at depressed prices or keep building cash. I would not double count that on top of the valuation math, but it is a nice problem to have.

And none of this includes Falcon. Agentic labor is the call option sitting on top. If Veeva can sell even a slice of the labor budget, this can move from a good investment to an exceptional one.

Pitfalls

AI accelerates research less than I think, and pharma throughput barely moves.

Downstream data automation gets captured by internal proprietary pharma tooling.

Seat compression bites before usage-based revenue scales to offset it.

Salesforce wins back meaningful CRM share on the commercial side.

Disclaimer: This article is for informational and educational purposes only. Do not interpret anything above as financial advice. Always do your own research before making any investment decision. This is NOT a buy or sell recommendation.

AlphaEvolve was applied to 50+ open problems in mathematics, matching state-of-the-art in ~75% and improving the best known solution in ~20%.